2023 - Same, Same

Work Please: AI, by NightCafe

2022 REDUX

In which I review my preview of India in Gimme Mo #6, entitled ‘Jokers in 2022’.

Quotes from that edition are in italics.

The Indian Economy in 2022

Everybody - OK, most everybody - believes that the Indian economy will grow at between 8% and 10% next year. I don’t.

Indeed, in 2022, expectations from the Indian economy have bent to reality, and the official estimate of GDP growth for the financial year ending on March 31st of this year is now 7%. This is, of course, the estimate for growth in the formal economy. As I wrote in Gimme Mo 3, the troubles of the informal sector have been deep and widespread, and our statistics have not been able to capture the extent of pain at the base of our economy. In other words, the growth of the Indian economy has been considerably lower than the official numbers, which only track the formal sector.

OMICRON

Though there is evidence that the new variant will be less lethal than Delta, if fresh cases spiral as they have in other nations, there will be a serious hiccup in economic activity, especially in the services sector. Consumer confidence, still at a low ebb, will definitely dip all over again, pushing recovery further out.

Omicron had little impact on the Indian economy. Consumer confidence did not dip, but has been very slow to recover. The latest RBI reading is 83, and a return to the pre-pandemic level of 100 seems a long way off. Employment numbers continue to be very sluggish, and the triggers for growth are elusive.

Inflation and Interest Rates

We don’t know which way Indian inflation is headed. Consumer price inflation is just below 5%, but wholesale inflation is over 14%, and at some point the two have to converge. Our easy money policy and low interest rate regime are both on edge, and money will get tighter if inflation keeps biting.

Inflation, as measured by the CPI index, did climb, but peaked at 7.8% in April of this year. and is now heading down. Wholesale inflation converged with retail inflation, and is now down to 5.85%, so the worst may be behind us.

The bigger part of the story is interest rates in the US.. Real-interest rates in the US are measured by the difference between the interest (or yield) on 1 year government bonds, and consumer inflation. With inflation at over 6%, this measure is at a 75-year low of -6.53%. Consumer inflation is way outside the comfort zone, so interest rates have to go up, but US policy makers would like to do this gradually, beginning in March. Charles Goodhart and Manoj Pradhan warn of the danger “that central banks might reverse policies suddenly and dramatically, with a 180-degree course correction entailing 50 basis point hikes and shrinking balance sheets.”

Rate hikes of 75 basis points (0.75%) were not even envisaged! But we saw 4 of them in the year, and US benchmark bond yields soared, from 1.63% to 4.25%, before falling back. This surge in returns on the ‘safest asset’ had a massive impact on the demand for risky assets all over the world, and most equity markets were deeply impacted, not least of all the tech-heavy Nasdaq, which lost 30%. Indian equities were more or less flat, which counts as a huge out-performance.

If (tightening were to happen), India would lose control of either its interest rate, or its currency, probably a mix of the two, and the chances of disorderly policy decisions would escalate. Sudden tightening in the US would have an unpredictable impact on our economy. I must repeat that I am not making a prediction here,

Accordingly, the Indian rupee lost significant ground against the dollar, moving from 74.50 to 82.5. From January to September, most currencies weakened against the dollar, a scenario best depicted by the dollar index, which surged from 96 to 114, a massive hardening of almost 19%. Since then, the US dollar has retreated by 9%, to 104, but the rupee continues to sag. The US Federal Reserve doesn’t look like it is done with interest rate hikes, so we will continue to see pressure on interest rates, the rupee, or both.

The bearish scenario for the rupee is reinforced by our trade deficit, which is at an all-time high. The export scenario continues to look bleak, so the only development which could offer some relief is a significant drop in crude prices. One can only hope.

The Eastern Sector

And the one who shall not be named.

I’m putting this down here, because a dragon-shaped joker could be the most potent one in the pack. But I think it will remain where it is, just peeking out from under the table cloth. Enough to remind us how vulnerable we are, to facilitate some more salami-slicing of Indian territory, but not a serious play, which would disrupt our pretence of normalcy at the border. If this reading is wrong, all bets are off.

This prediction was bang on. Our government would like to pretend that all is well at the Chinese border, but has had to gradually move to an admission of some trouble, because a few - very few - media commentators have continually highlighted the loss of patrolling rights for the Indian army, and grazing rights for Ladakh herders. I would still like to believe that the Chinese will not make a serious play for substantial Indian territory, but the PLA is definitely upping its salami slicing game, while putting down massive infrastructure all along our eastern borders.

STOCK MARKETS

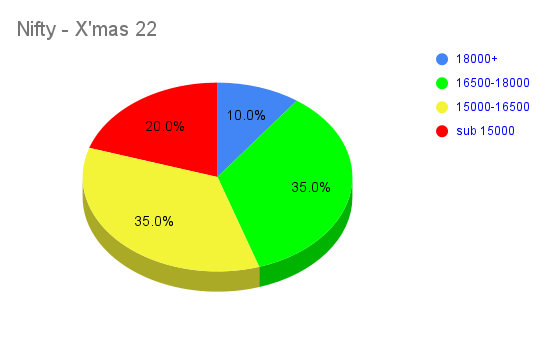

I said I wouldn’t make any predictions about the economy here, but I do take real life bets on the Indian stock-markets. The NIFTY closed just above 17,000 on Friday (December 24, 2021) and here is my dart-board assigning probabilities to where it could be a year from now:

Looking back, this chart had little predictive content - the Nifty could have been anywhere between 15000 and 18000, and I could have said - “told you so”.

2023 is full of unknowns - especially around global liquidity and geo-politics - so it would be a fool’s game to put a sharper number on the performance of the Indian market this year. But I will play that fool, and hazard that the Nifty will end the year lower than where we began. My target landing zone for the Nifty on December 31st 2023 is 16000 to 16500.

Economic Narrative

Till I read my comments from a year ago, I didn’t realise how much the economic narrative has shifted in one year. From aggressive tom-tomming of an economy bouncing back, the regime has turned increasingly defensive, especially in the last few weeks. The communications task now is to deflect blame from the government’s economic policy errors - demonetisation, ill-administered GST, and thoughtless lockdowns - to the impact COVID has had on all economies. The deepening crisis in unemployment, too, some commentators would have us believe, has nothing to do with the policy choices of the government, but comes from the technological forces that rule the world.

It is true that you can no longer produce cars without robots, or erect skyscrapers with bricks carried by the headload, but this deflection is not even deft. Whether cars or buses, skyscrapers or budget housing, India needs more economic activity at every level, with more people wielding shovels, operating cranes, or installing high capacity routers. Rather than finding excuses for low growth, our government needs much more potent plans to energise economic activity.

For the last couple of years, the Indian government has tried to buoy the economy by a high level of capital expenditure, in infrastructure. The most visible sign of this is the build-out of roads across the country. However, this has come at the cost of high government deficits. The sense one gets from the official narrative is that this cannot continue for much longer. Private sector investment, we are now being told, must do the heavy lifting.

I am pretty clear that we are not going to see that in 2023, which is as far as the scope of this post extends. The mood of most businessmen is watchful, rather than optimistic, and I see little chance of a surge in investment activity in the next twelve months. Between the fiscal constraints of the government, the wary stance of corporates, and the beaten-down confidence of the Indian consumer, it’s going to be another slow year for the Indian economy.

2020 and 2021 were stellar.

2022 was flat.

Thanks, Ranjan.

Unfortunately, the wiggle room is very limited now, with the major fiscal constraints, and the global scenario so uncertain. We will just muddle along for a couple of years.