#6 Jokers in 2022, and Other Black Tales

There’s more…

Cruel Jokes in 2022

Everybody - OK, most everybody - believes that the Indian economy will grow at between 8% and 10% next year. I don’t.

That’s not because I have a different number, but because I think that there are too many jokers in the hand to call out the arc of the Indian economy. As the year plays out, if these wild cards find their way into the game, the course of our economy can take a few twists. I’m not going to make any predictions then, but point to some of these key concerns, and suggest how they could impact us.

OMICRON

By Diwali, COVID had ceased to be a factor in Indian economic activity. The malls were full, the roads were packed, and Delhi’s smog was back with a vengeance. Our vaccine drive lost a sense of urgency: against a year-end target of 100%, only 60% of Indian adults had been fully vaccinated by the end of last week. The reluctant opening of our schools and colleges was really the last vestige of COVID-altered behaviour. Now Omicron could upend everything.

Though there is evidence that the new variant will be less lethal than Delta, if fresh cases spiral as they have in other nations, there will be a serious hiccup in economic activity, especially in the services sector. Consumer confidence, still at a low ebb, will definitely dip all over again, pushing recovery further out.

Even if India escapes with a relatively low health impact, global supply chains (I rarely heard that term before last year) are already backing up again. Ocean freight costs on key routes went up 5-fold in 2021, and trade experts now believe that they will not settle before mid-2022. Fresh containment measures in China and the US will make things worse. Imported inflation and lower domestic activity make for a terrible combination.

Interest Rates

We don’t know which way Indian inflation is headed. Consumer price inflation is just below 5%, but wholesale inflation is over 14%, and at some point the two have to converge. Our easy money policy and low interest rate regime are both on edge, and money will get tighter if inflation keeps biting. This is only one part of the story, though.

The bigger part of the story is interest rates in the US. As long as they have remained low, money has bounced around the world in the “search for yield”, meaning higher returns than the near-zero available in the US. This can change fast. Real-interest rates in the US are measured by the difference between the interest (or yield) on 1 year government bonds, and consumer inflation. With inflation at over 6%, this measure is at a 75-year low of -6.53%. Consumer inflation is way outside the comfort zone, so interest rates have to go up, but US policy makers would like to do this gradually, beginning in March. But these same folks have recently had to abandon their stance that inflation is transitory, and advance their plans to taper bond-buying. Charles Goodhart and Manoj Pradhan warn, on VOX EU, of the danger “that central banks might reverse policies suddenly and dramatically, with a 180-degree course correction entailing 50 basis point hikes and shrinking balance sheets.”

This has happened before. Between March and October of 1980, US real interest rates had also been negative, hitting a low of -5.7%. But matters went out of hand, consumer inflation surged to 13%, and interest rates had to be raised in giant steps. By September 1981, the 1 year bond carried a yield of over 15%.

If something like this were to happen again, India would lose control of either its interest rate, or its currency, probably a mix of the two, and the chances of disorderly policy decisions would escalate. Sudden tightening in the US would have an unpredictable impact on our economy. I must repeat that I am not making a prediction here, just reminding myself that we have never before witnessed such a flood of money, and are not well-placed to predict the fall-out of its withdrawal.

Data

We’re still arguing about how much the Indian economy grew before COVID hit. In a controversial paper published in 2019, Arvind Subramanian asserted that our official statistics were over-estimating GDP growth. Drawing on aggregates like electricity generation and sales of commercial vehicles, he believed that the new GDP series introduced in 2015 over-estimated our growth by 2.5%*. Having been our Chief Economic Advisor from 2014 to 2018, his views carried credibility, and the Economic Survey of 2019-20 found it necessary to try and prove him wrong.

I believe we have serious data problems. In the third edition of this newsletter, I wrote that the troubles of the informal sector have been deep and widespread, and our statistics have not been able to capture the extent of pain at the base of our economy.

I’m hearing that Lutyen’s Delhi is slowly waking up to the realisation that All is Not Well with the Indian economy. But without accurate data, especially on the informal sector, economic policy-makers will be flying blind. Second-order data, like GST collections, or sentiment-driven numbers, like the NIFTY, are good for headlines, but we need much sharper readouts on economic activity to drive decision-making.

The Eastern Sector

And the one who shall not be named.

I’m putting this down here, because a dragon-shaped joker could be the most potent one in the pack. But I think it will remain where it is, just peeking out from under the table cloth. Enough to remind us how vulnerable we are, to facilitate some more salami-slicing of Indian territory, but not a serious play, which would disrupt our pretence of normalcy at the border. If this reading is wrong, all bets are off.

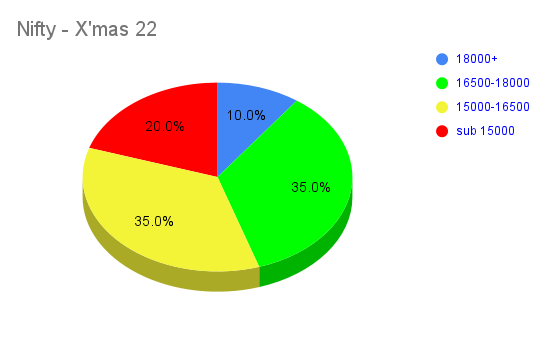

I said I wouldn’t make any predictions about the economy here, but I do take real life bets on the Indian stock-markets. The NIFTY closed just above 17,000 on Friday, and here is my dart-board assigning probabilities to where it could be a year from now:

The Power of Narrative

In October 1992, I visited Chakori, in the far north of Uttarakhand. From a knoll in the forest, we watched the sunset over the Panchuli peaks, then clambered down to the road, towards the police chowki. An electric heater glowed orange, and we could hear the news over the radio. The door was ajar, so we waved hello, and the policeman invited us in. I shared a bidi with him, and listened to news of kar-sevaks massing in Ayodhya. On the darkening road, a bus rolled to a stop.

“Give me a minute”, he said, “there’re just two buses a day, and I need to keep a tab on them”.

“We hardly saw any traffic on our way here”, I said when he returned. “Do the buses have many passengers?”

“At this time of year, not normally. But this year, every village - even those deep down in the valleys - is sending a couple of young men to Ayodhya, to build the Ram Mandir.”

I asked him what he thought about the movement.

“Of course we must build a Ram Mandir there - it is the birthplace of our Bhagwan Ram”

“Sure, but is it necessary to destroy one place of worship to build another?”

“Absolutely. They have imprisoned our Lord Shiva; they must pay the price.”

I was lost.

“The black stone they have in Mecca – that is a Shivling. He shrieks at night, asking to be returned to his followers. If we cannot get him back, then we must inflict damage on them. We cannot be dumb spectators to the insults to our religion. They must know that we too have the ability to fight back.”

The narrative, and the ability to mobilise around that narrative - these are the key to political victory, the truth be damned. Thirty years ago, in a cold, remote spot in the Kumaon, I first experienced the ability of a political movement to spin a story out across the nation, to rouse anger and self-righteousness.

Other political movements have a lot to learn.

Sunset at Chakori

TILpiece

In a certain southern state, I believe contractors to the Public Works Department are now expected to kick-back 30% of the value of any contract. A substantial percentage of this must be paid before the contract is awarded. Larger contractors have the cash flow to feed the beast. But those trying to shimmy up the pole from Class 4 contractors all the way to Class 1, struggle with this funding requirement.

I learned last week how considerate the public engineers have become. They will introduce ambitious, upwardly mobile contractors to financiers, who fund the up-front ‘facilitation fee’, and keep the wheels of commerce moving.

Fintech with the public interest at heart.

It was great read, especially the the narrative one .

Thanks Mohit for a wonderful write-up.

I almost fell off reading the last bit from the newsletter - about the kick-backs in PWD. Well, I am myself a PWD contractor based in Jharkhand, and I can confirm that kick-backs are a routine thing for us, but 30% sounded like an extreme case (unless this is one of those cases where the payment will be made without any actual work being done....yeah, that happens too, and in such cases people end up sharing 50:50 ;) )

[I will take a moment to let you know that I have been a keen follower of your work, and value your vast experience. I first heard you on Amit's podcast and since then I have been trying to follow everywhere you leave your digital footprints.]

Have a great day!